Global Industrial Wireless Communication Market: Regional Analysis & Opportunities

Blog 2026-07-04

Global Industrial Wireless Communication Market: Regional Analysis & Opportunities

Key Overview

Target Audience: Global market development professionals, international business managers, wireless equipment exporters, cross-border defense and industrial communication solution providers

Core Question: What is the current state of the global industrial wireless communication market? What are the characteristics and opportunities of each regional market? How to formulate a global market entry strategy?

Key Conclusion: The global industrial wireless communication market is growing rapidly, with Asia Pacific, North America, Europe, and the Middle East being the main markets. Entering the global market requires understanding regional regulatory and certification requirements, establishing localized distribution channels, and adjusting product strategies for different regions.

Global Industrial Wireless Communication Market Overview

Industrial wireless communication has transitioned from a niche technology for specialized applications to the backbone of modern industrial digitalization. Unlike consumer WiFi networks that prioritize coverage and convenience, industrial wireless networks must deliver deterministic latency (sub-10ms for real-time control applications), carrier-grade reliability (99.999% uptime equivalent to wired networks), and robust operation in electrically hostile environments with wide temperature ranges (-40°C to +75°C), high vibration, and electromagnetic interference from heavy machinery. These requirements drive a distinct technology ecosystem with higher-value products and longer lifecycle support compared to the consumer market.

The market’s growth trajectory is fundamentally shaped by three structural drivers. First, the global installed base of industrial IoT devices is expected to reach 37 billion connections by 2027 (IoT Analytics), each requiring reliable wireless backhaul for data collection and command delivery. Second, the transition from proprietary industrial protocols (Profibus, Modbus RTU, CAN bus) to IP-based wireless networking (WiFi 6, 5G NR-U, WirelessHART) is opening new deployment scenarios that were previously considered too demanding for wireless — including real-time robot control, AGV fleet management, and closed-loop process control. Third, the declining cost of industrial-grade wireless hardware (driven by commercial chipset volumes and improved manufacturing yields) has reduced the total cost of ownership for wireless deployments to within 15-25% of equivalent wired installations, making wireless the economically preferred option for new factory builds and brownfield retrofits alike.

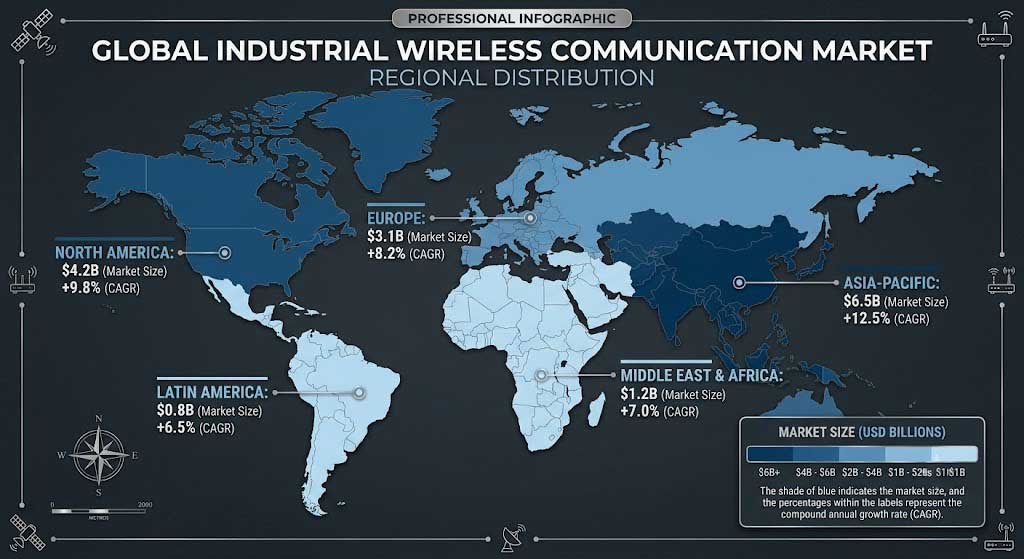

Global Market Size and Growth by Region

| Region | Market Size (2024) | Projected (2030) | CAGR | Primary Growth Drivers |

|---|---|---|---|---|

| Asia Pacific | $6.5B | $17.5B | 18% | Manufacturing automation, smart city megaprojects, 5G industrial deployment (China, South Korea, Japan) |

| North America | $4.2B | $8.3B | 12% | Industrial IoT platform adoption, oil & gas digitization, reshoring-driven factory modernization |

| Europe | $3.1B | $5.5B | 10% | Industry 4.0 policy frameworks (Germany Industrie 4.0, UK Made Smarter), green energy transition |

| Middle East & Africa | $1.2B | $2.8B | 15% | Oil & gas facility digitization, NEOM and other smart city projects, mining automation in South Africa |

| Latin America | $0.8B | $1.8B | 14% | Precision agriculture IoT, mining automation (Chile, Peru), logistics modernization in Brazil |

Key Market Trends Reshaping Industrial Wireless

Five technology trends are fundamentally reshaping the industrial wireless landscape, creating both opportunities and requirements for equipment manufacturers and system integrators. Understanding these trends is essential for product roadmap planning and market positioning.

Private 5G and 5G NR-U (5G New Radio Unlicensed): The emergence of private 5G networks — using either licensed spectrum (CBRS in the US, local licenses in Germany and Japan) or unlicensed 5G NR-U in the 5GHz and 6GHz bands — is creating a new tier of industrial wireless capability. Private 5G offers deterministic latency under 1ms, massive device density (1 million devices per square kilometer), and network slicing for quality-of-service guarantees. Early adopters in automotive manufacturing (BMW, Volkswagen) and port logistics (Hamburg Port Authority) have demonstrated 99.999% reliability in production environments. The private 5G infrastructure market is projected to grow from $1.2B in 2024 to $8.5B by 2030 at 39% CAGR.

WiFi 6/6E (802.11ax) Adoption in Industrial Settings: WiFi 6 is replacing legacy WiFi 4/5 in industrial environments at an accelerating rate, driven by four key capabilities: OFDMA (Orthogonal Frequency Division Multiple Access) that reduces latency to under 5ms for industrial control traffic, MU-MIMO that supports up to 8 simultaneous device transmissions, target wake time (TWT) that extends battery life for IoT sensors, and 6GHz band support (WiFi 6E) that provides 1,200MHz of clean spectrum for interference-free operation. Industrial WiFi 6 access point shipments are expected to grow 35% annually through 2028.

Edge Computing and Distributed Intelligence: The centralization of industrial control systems is giving way to edge computing architectures where data processing occurs at or near the wireless access point. Modern industrial wireless bridges and APs increasingly integrate compute modules (ARM Cortex-A72 or x86-based) capable of running containerized applications for data pre-processing, protocol translation, and local decision-making. This reduces cloud dependency, lowers operational latency, and enables functionality during WAN outages. The industrial edge computing market is projected to reach $15.2B by 2028.

AI/ML Integration for Predictive Maintenance and Network Optimization: Machine learning algorithms are being deployed on industrial wireless networks for two primary use cases: predictive maintenance that analyzes RF signal patterns to detect degrading hardware before failure, and dynamic spectrum optimization that autonomously selects channels and modulation schemes based on real-time interference analysis. Early implementations have demonstrated a 40-60% reduction in unplanned network downtime and 15-20% throughput improvement in congested RF environments.

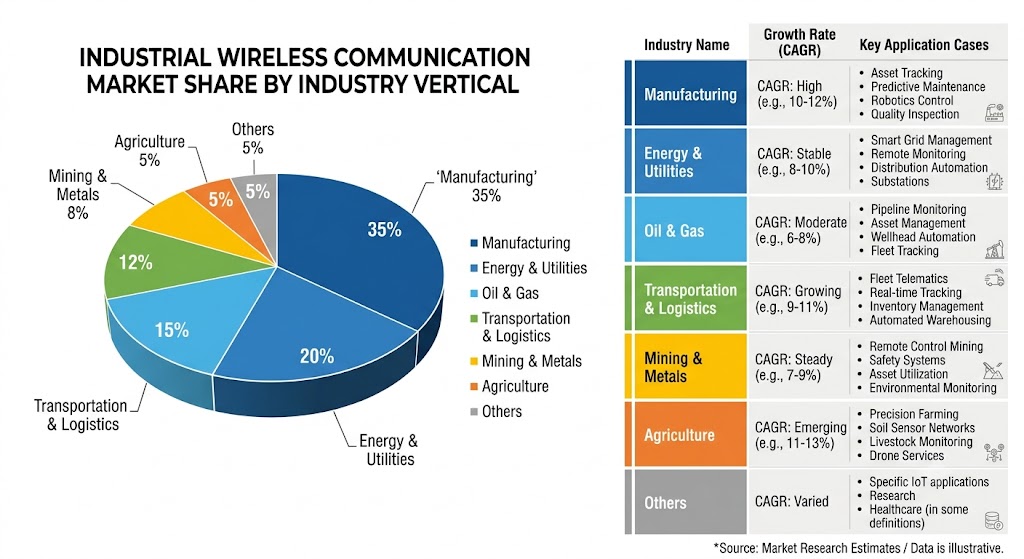

Growth Drivers by Industry Vertical

Manufacturing accounts for 35% of industrial wireless spending, making it the largest vertical, while transportation and logistics are the fastest-growing segments at 18% CAGR. Each vertical has distinct requirements that influence product selection, deployment architecture, and certification needs.

| Industry Vertical | Market Share (2024) | Growth Rate | Primary Wireless Application | Key Technical Requirement |

|---|---|---|---|---|

| Manufacturing & Automotive | 35% | 14% | AGV communication, robot control, production line monitoring | Sub-10ms latency, 99.999% reliability |

| Energy & Utilities | 20% | 13% | Smart grid backhaul, substation automation, renewable asset monitoring | IEC 61850 compliance, long-range (10-30km) |

| Oil & Gas | 15% | 11% | Pipeline monitoring, wellhead automation, refinery asset tracking | Hazardous location rating (ATEX/UL), extreme temperature range |

| Transportation & Logistics | 12% | 18% | Port automation, warehouse robotics, railway communication | High client density (500+ devices per AP), seamless roaming |

| Mining & Metals | 8% | 15% | Autonomous haulage, ventilation control, personnel tracking | NLOS mesh networking, ruggedized hardware |

| Agriculture | 5% | 20% | Precision irrigation, drone control, equipment telemetry | Solar-powered operation, multi-kilometer range |

| Other (Smart Cities, Public Safety) | 5% | 12% | Traffic management, surveillance backhaul, emergency communication | Encrypted communication, redundant link failover |

Regional Market Analysis

Asia Pacific — The Largest and Fastest-Growing Market

Asia Pacific dominates the global industrial wireless market with $6.5 billion in 2024 (41% of global total) and the highest regional growth rate at 18% CAGR, driven by China’s manufacturing automation push, India’s industrial digitization programs, and Southeast Asia’s rapid infrastructure development. The region’s growth is fundamentally structural rather than cyclical: rising labor costs in China and Vietnam are forcing manufacturers to automate, while government initiatives like “Made in China 2025” and “Digital India” provide policy support and funding for industrial digitalization projects.

China alone accounts for approximately 45% of the Asia Pacific industrial wireless market, with demand concentrated in electronics manufacturing (Shenzhen, Suzhou), automotive production (Shanghai, Guangzhou), and smart city infrastructure. The Chinese market has unique characteristics: a strong preference for domestic suppliers when certification and performance are comparable, strict spectrum regulations that limit 5GHz outdoor use to 5150-5350MHz only, and CCC (China Compulsory Certification) and SRRC (State Radio Regulation) requirements that add 10-16 weeks to market entry timelines. Foreign manufacturers face additional challenges including localization requirements, data sovereignty regulations, and the need for guanxi (relationship-based) business development.

Southeast Asian markets — particularly Vietnam, Thailand, and Indonesia — are emerging as high-growth opportunities driven by supply chain diversification from China. Vietnam’s industrial wireless market is growing at 22% CAGR, fueled by Samsung’s electronics manufacturing complex (the company’s largest smartphone factory globally), growing textile and footwear automation, and investments in port logistics at Haiphong and Ho Chi Minh City. These markets have less restrictive certification requirements (many accept CE or FCC with local documentation supplements) and lower price sensitivity, making them attractive entry points for new market participants.

North America — Mature Market with Advanced Application Focus

North America represents the second-largest regional market at $4.2 billion, with a 12% CAGR driven by industrial IoT platform adoption, oil and gas facility modernization, and reshoring of manufacturing capacity from Asia. The US market is characterized by the highest average selling prices for industrial wireless equipment (20-30% above Asia Pacific equivalents), reflecting customer willingness to pay for reliability, certification compliance, and after-sales support. FCC certification is the most established regulatory framework globally, with well-defined testing protocols and mutual recognition agreements with Canada (ISED) that simplify North American market access.

The US industrial wireless market is segmented into three distinct sub-markets: large enterprises (Fortune 500 manufacturers, oil majors) that require carrier-grade solutions with 5-year support commitments and on-site engineering services; mid-market industrial companies that seek proven solutions with distributor-provided integration services; and system integrators who specify wireless equipment for client projects and value technical documentation and vendor training programs. Each segment requires a different go-to-market approach: direct sales with solutions engineering for enterprise, two-tier distribution for mid-market, and technical partner programs for system integrators.

Canada’s market, while smaller at approximately $700 million, offers attractive opportunities in natural resource sectors — mining (Sudbury, Alberta oil sands), forestry (British Columbia), and hydroelectric power (Quebec) — where long-range wireless communication is essential for remote site connectivity. Canadian customers typically prefer suppliers who maintain local inventory and technical support presence, given the country’s geography and time zone considerations.

Europe — Sustainability-Driven Market with Strong Regulatory Framework

Europe’s $3.1 billion industrial wireless market grows at a more moderate 10% CAGR but commands premium pricing due to stringent regulatory requirements (CE RED, ErP, RoHS, REACH), strong sustainability mandates, and the influence of the Industry 4.0 policy framework. The European market is unique in its emphasis on energy efficiency — the ErP Directive (Energy-related Products) imposes standby power consumption limits that affect product design, while corporate sustainability reporting requirements drive demand for energy-monitoring wireless sensor networks.

Germany is the largest European market (28% of regional total), driven by its world-leading automotive and industrial automation sectors. German customers are characterized by rigorous technical evaluation processes (typically requiring 3-6 months of product testing before vendor qualification), preference for engineering-led sales approaches, and willingness to pay premium prices for demonstrated reliability. France and the UK are the second-tier markets, each at approximately $500 million, with stronger price sensitivity and faster adoption of cloud-managed wireless solutions compared to Germany’s preference for on-premise management.

Eastern European markets — Poland, Czech Republic, Romania — are growing rapidly (15-18% CAGR) as manufacturing capacity shifts from Western Europe to lower-cost locations. These markets are more price-sensitive but offer faster decision cycles and less stringent vendor qualification processes. The CE RED certification obtained for Western Europe is valid across all EU member states, providing a regulatory foundation for pan-European market access.

Middle East & Africa — High-Growth Opportunity in Oil & Gas and Smart Cities

The Middle East and Africa market, valued at $1.2 billion with 15% CAGR, is driven by oil and gas facility digitization in the Gulf Cooperation Council (GCC) countries and smart city megaprojects including Saudi Arabia’s NEOM and the UAE’s Masdar City. The Middle East market is characterized by project-based demand — large, multi-year infrastructure programs rather than recurring operational spending — which creates lumpy revenue patterns but high-value opportunities for suppliers with strong project management and local partnership capabilities.

Saudi Arabia’s industrial wireless market is the largest in the region, driven by Vision 2030’s industrial diversification programs and the development of new economic zones (RASIN, King Abdullah Economic City). CITC (Communications and Information Technology Commission) certification is required, with specific requirements for spectrum bands used in oil and gas telemetry. The UAE market focuses on smart city infrastructure in Dubai and Abu Dhabi, with strong demand for outdoor WiFi 6 APs, mesh networks for facility management, and long-range wireless bridges for pipeline and utility monitoring.

Africa’s market is smaller but growing rapidly from a low base, with concentrations in South Africa (mining automation), Nigeria (oil and gas), and Kenya (agriculture IoT). The African market presents unique challenges: unreliable grid power necessitates solar-powered solutions, limited local technical support requires remote management capabilities, and fragmented regulatory frameworks across 54 countries complicate pan-African product certification. Suppliers who address these challenges with appropriate product adaptations gain significant competitive advantage.

Latin America — Emerging Opportunity in Agriculture and Mining Automation

Latin America’s $800 million industrial wireless market grows at 14% CAGR, driven by precision agriculture in Brazil and Argentina, mining automation in Chile and Peru, and logistics modernization across the region. Brazil is the largest market (40% of regional total), requiring ANATEL certification for wireless equipment — a process that typically takes 8-16 weeks and requires in-country testing for some product categories. The Brazilian market is characterized by high import duties (30-60% on electronics) that favor local assembly or partnership models over direct import.

Chile and Peru represent high-growth mining automation opportunities, with copper and lithium mining operations deploying autonomous haulage systems, remote monitoring, and personnel safety tracking that require reliable wireless communication in challenging underground and open-pit environments. These applications demand ruggedized equipment (dust, vibration, extreme temperature), long-range NLOS capability (for underground tunnels), and integration with mine management systems. Suppliers with experience in industrial mining wireless applications have a distinct advantage in these markets.

Argentina and Colombia offer growing agriculture IoT opportunities, with precision irrigation systems, crop monitoring sensors, and equipment telemetry deployed across large agricultural operations. These applications require cost-effective solutions with multi-kilometer range (typical farms span 500-5,000 hectares), solar-powered operation (grid power is often unavailable in rural areas), and support for common agricultural protocols (NMEA 0183 for GPS, ISOBUS for equipment integration).

Global Regulatory Environment and Certification Requirements

Frequency Allocation by Region — Critical Differences That Affect Product Design

While the 2.4GHz ISM band (2400-2483.5MHz) is harmonized globally with near-uniform regulations, the 5GHz band (5150-5850MHz) is fragmented across regions, requiring either multi-band radio designs or region-specific SKUs. This fragmentation is the single most important factor in determining whether a wireless product can be sold globally with a single hardware design or requires regional variants.

| Region | 2.4GHz (2400-2483.5MHz) | 5GHz Low (5150-5350MHz) | 5GHz Mid (5470-5725MHz) | 5GHz High (5725-5850MHz) | Special Bands |

|---|---|---|---|---|---|

| US (FCC) | Up to 1W EIRP, unrestricted | UNII-1: Indoor only, up to 50mW/MHz | UNII-2/2e: DFS required, up to 250mW/MHz | UNII-3: Up to 1W EIRP, no DFS | 900MHz ISM (FHSS only), 6GHz (UNII-5/6/7/8) |

| Canada (ISED) | Up to 1W EIRP | Harmonized with FCC UNII-1 | Harmonized with FCC UNII-2/2e | Harmonized with FCC UNII-3 | 6GHz band (pending) |

| EU (CE RED) | Up to 100mW EIRP (20dBm) | Indoor only, up to 200mW EIRP | DFS + TPC required, up to 1W EIRP | Low power (25mW) or SRD | 5.8GHz band restricted |

| China (CCC/SRRC) | Up to 100mW EIRP | 5150-5350MHz only, indoor, low power | Not allowed | 5725-5850MHz, low power (25mW) | 2.4GHz only for outdoor bridges |

| Japan (TELEC/MIC) | Up to 100mW EIRP | W52 (5150-5250MHz): Indoor | W53 (5250-5350MHz): DFS, W56 (5470-5725MHz): DFS | W59 (5725-5850MHz): Limited | 4.9GHz band for industrial |

| Australia (ACMA) | Up to 4W EIRP | Indoor only | DFS required | Up to 4W EIRP for point-to-point | 5.8GHz allowed for fixed links |

Key Certification Requirements by Market

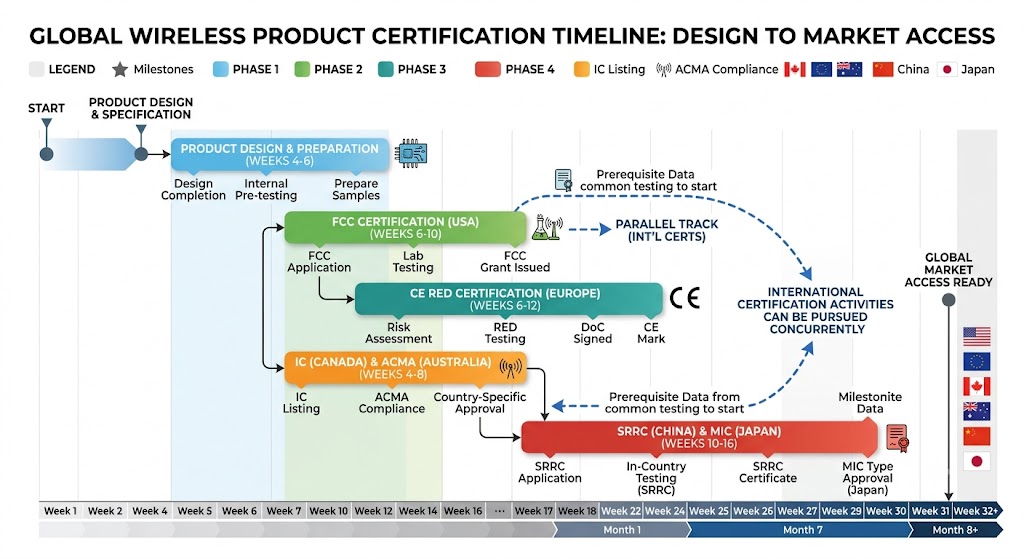

Each target market requires specific certifications that address radio frequency compliance, electromagnetic compatibility (EMC), electrical safety, and environmental impact (RoHS/REACH). The certification process typically takes 6-16 weeks per market and costs $8,000-$25,000 for the initial product variant, with subsequent variants (different enclosure, antenna configuration) costing less if the core radio design is unchanged.

| Market | Radio Certification | EMC/Safety Standards | Testing Requirement | Typical Timeline |

|---|---|---|---|---|

| United States | FCC Part 15.247/15.407 | FCC Part 15B (EMC) | FCC-recognized lab (TCB) | 6-10 weeks |

| Canada | ISED RSS-247/RSS-210 | ICES-003 (EMC) | FCC/ISED-recognized lab | 4-8 weeks (can combine with FCC) |

| European Union | CE RED 2014/53/EU | EN 301 489 (EMC), EN 62368-1 (Safety) | Notified Body or self-declaration | 6-12 weeks |

| China | SRRC (radio) + CCC (EMC/safety) | GB/T 9254 (EMC), GB 4943.1 (Safety) | In-country testing required | 10-16 weeks |

| Japan | TELEC (MIC Ordinance) | VCCI (EMI), PSE (Safety) | Registered lab (local or Japan-recognized) | 8-12 weeks |

| South Korea | KC (MSIP) certification | KC EMC, KC Safety | Korea-recognized lab required | 8-12 weeks |

| Australia/New Zealand | ACMA RCM (AS/NZS 4268) | AS/NZS CISPR 22 (EMC) | Accredited lab, no local requirement | 4-8 weeks |

| Brazil | ANATEL Resolution 529 | ANATEL EMC + Safety | In-country testing for Type I products | 8-16 weeks |

| Saudi Arabia | CITC certification | IEC/EN standards accepted | Local representative required | 4-8 weeks |

| UAE | TRA certification | IEC/EN standards accepted | Local representative required | 4-8 weeks |

Global Certification Strategy — Optimizing Cost and Timeline

An optimized certification strategy begins with designing a single RF platform that can be configured for multiple regulatory domains through firmware-controlled parameters (TX power limits, channel lists, DFS behavior) rather than hardware changes. This “one hardware, multiple firmware” approach reduces the number of certification testing cycles from N (one per region) to 2-3 (one per major radio variant) and saves $20,000-$50,000 in total certification costs for a 5-market launch.

Certification sequencing matters. FCC certification should typically be obtained first because: (1) FCC has the most rigorous and well-defined testing methodology, (2) FCC results can often be leveraged for ISED (Canada) through the FCC-ISED MRA (Mutual Recognition Agreement), saving $3,000-$5,000 and 2-3 weeks, and (3) FCC test reports are accepted as supporting documentation by several other regulatory bodies. CE RED certification for Europe should follow, as the harmonized standards (EN 301 893 for 5GHz, EN 300 328 for 2.4GHz) overlap significantly with FCC testing — typically 60-70% of FCC test results can be reused for CE RED submission, with the remaining 30-40% covering EU-specific requirements (ErP standby power, additional DFS tests, lower TX power verification).

China (CCC/SRRC) and Japan (TELEC) are the most challenging certifications, requiring local testing through accredited laboratories in each country. These certifications should be planned for Phase 2 of market expansion (years 2-3) rather than Phase 1 launch, unless China or Japan are primary target markets. The total certification budget for global coverage across 5 major markets (US, EU, Canada, Australia, China) typically ranges from $50,000 to $85,000 for a single product platform with two variants (2.4GHz + 5GHz), assuming pre-compliance screening catches 90%+ of issues before formal testing.

Recommended Wireless Solutions by Region

The selection of the right wireless solution platform for a given regional market depends on three factors: frequency band availability (determined by local regulations), environmental requirements (temperature range, IP rating, surge protection), and application-specific performance needs (throughput, range, latency, client capacity). Zukaka’s product portfolio covers all major deployment scenarios with platforms that have been pre-validated for FCC, CE, and ACMA compliance, with documented modification pathways for China (CCC/SRRC), Japan (TELEC), and other regional certifications.

Industrial Wireless Bridge Solutions by Deployment Scenario

For point-to-point and point-to-multipoint bridge deployments, the choice of platform is primarily determined by range requirements and regional frequency regulations. The 11ac 24V platform is optimized for medium-range links (up to 10-15km) in industrial environments where 24V DC power is readily available, while the 11ac 48V platform supports long-range links (up to 30km) with PoE convenience and integrated surge protection for outdoor tower or rooftop installations.

| Platform | Best For | Regional Certification Status | Key Regional Adaptation |

|---|---|---|---|

| 11ac 24V Gigabit Bridge PCBA | Factory automation, warehouse backhaul, campus connectivity (500+ Mbps, 10-15km, IP65, -40°C to +75°C) | FCC, CE, ACMA base compliance | Firmware-region locked TX power; EU variant with ErP-compliant standby power (<1W) |

| 11ac 48V Long-Range Bridge PCBA | Oil & gas pipeline monitoring, mining, utility backhaul (500+ Mbps, 30km, 48V PoE, surge protection) | FCC, CE, ACMA base compliance | China variant with 2.4GHz-only operation (CCC/SRRC); Japan variant with W56 DFS support (TELEC) |

| 11n 24V Wireless Bridge PCBA | Cost-sensitive deployments in emerging markets (150+ Mbps, up to 10km, basic environmental protection) | FCC, CE base compliance | Unlicensed band operation for markets without strict 5GHz regulation; ideal for Latin America and Africa |

Recommended Solutions by Application and Region

Different regional markets prioritize different wireless applications based on their industry structure and infrastructure development stage. The following application-to-solution mapping considers both technical requirements and regional feasibility.

| Application | Recommended Solution Platform | Primary Target Regions | Key Technical Requirement | Certification Priority |

|---|---|---|---|---|

| Factory automation & AGV communication | WiFi 6 AP + 11ac 24V Bridge | Asia Pacific (China, Korea, Japan), Europe (Germany), North America | Sub-10ms latency, seamless roaming, 500+ devices per AP | FCC + CE (dual certification for global factory deployments) |

| Oil & gas pipeline monitoring | 11ac 48V Long-Range Bridge | Middle East (Saudi Arabia, UAE), North America (Canada oil sands), Russia | 30km range, ATEX/UL hazardous location rating, -40°C to +75°C | CITC (Saudi), TRA (UAE), FCC for North America |

| Smart grid & substation automation | 11ac 48V Bridge + Mesh motherboard | Europe (Germany, UK), North America, Asia Pacific (Japan) | IEC 61850 compliance, redundant link failover (<50ms) | CE RED (EU), FCC (US), TELEC (Japan) |

| Mining automation (underground & open-pit) | YN300A Mesh + 11ac 24V Bridge | Australia, South America (Chile, Peru), Africa (South Africa) | NLOS mesh for underground tunnels, ruggedized IP65, solar-compatible power | ACMA (Australia), ANATEL (Brazil) |

| Smart city & public Wi-Fi | Outdoor WiFi 6 AP + 11ac Backhaul | Middle East (UAE, Qatar), Asia Pacific (China, Singapore), Europe | High client density, 24/7 operation, centralized management | CE RED (EU), TRA (UAE), CCC (China) |

| Precision agriculture | 11n 24V Bridge (solar-powered) | Latin America (Brazil, Argentina), India, Africa (Kenya) | Solar-compatible (12V/24V DC), 5-20km range, low power consumption | ANATEL (Brazil), CE (for export markets) |

Regional Product Adaptation Guidelines

Products destined for different regions typically require three types of adaptation: regulatory (TX power, channel availability, DFS behavior), environmental (temperature range, IP rating, surge protection), and commercial (packaging, documentation, localization). Understanding which adaptations are mandatory versus optional helps optimize the cost of regional variants.

| Adaptation Type | US/Canada | Europe | China | Japan |

|---|---|---|---|---|

| TX Power Limit | Up to 1W EIRP (5.8GHz UNII-3) | Lower: 100mW (2.4GHz), 200mW-1W (5GHz with TPC) | 100mW (2.4GHz), very low 5GHz | 100mW (2.4GHz), W52/W53/W56 specific |

| 5GHz DFS | Required for UNII-2/2e | Required for 5470-5725MHz | N/A (most 5GHz bands not available) | Required for W53 and W56 |

| EIRP Limit (5GHz Bridge) | Up to 53dBm EIRP (high-gain antenna >23dBi exempt) | Up to 30dBm EIRP for point-to-point | Effectively 2.4GHz only for outdoor | Up to 30dBm EIRP with TPC |

| Temperature Range | Standard -20°C to +60°C (industrial -40°C to +75°C optional) | Same as US | Same as US | Same as US |

| Surge Protection | IEC 61000-4-5 Level 2 (standard), Level 3 (optional) | Same as US | GB/T 17626.5 equivalent | JIS equivalent |

| Documentation Language | English | Multi-language (EN + DE/FR/IT/ES) | Chinese (Mandarin) | Japanese |

Global Market Entry Strategy

Phase 1: Beachhead Markets (Year 1) — Establish Regulatory and Commercial Foundation

Year 1 should focus on 2-3 markets with well-defined certification processes, established distribution channels, and English-language business environments that minimize market entry friction. The United States is the recommended first market for most industrial wireless companies due to: the most straightforward FCC certification process globally (6-10 weeks with clear testing protocols), the largest single-country market for industrial wireless ($4.2B), and a mature two-tier distribution ecosystem (distributors + value-added resellers) that reduces the need for direct sales presence. FCC certification obtained for the US market also provides the foundation for ISED (Canada) certification through the mutual recognition agreement, effectively opening the North American market with a single certification investment.

Europe (CE RED) should be the second market priority. CE certification provides access to 27 EU member states plus EEA countries (Norway, Iceland, Liechtenstein) under a single certification, making it the most efficient multi-country market access mechanism available. The recommended entry point within Europe is either the UK (English-language, sophisticated logistics infrastructure, strong industrial IoT adoption) or Germany (largest European industrial market, engineering-led sales culture, premium pricing tolerance). A single distributor covering the UK, Germany, and Benelux markets can provide initial market coverage of approximately 45% of the European industrial wireless market.

Entry method for beachhead markets should be direct export through established distributors. This requires minimal upfront investment ($30,000-$50,000 for initial inventory, certification, and marketing materials) and allows the company to validate product-market fit before committing to more expensive local presence models. Key success metrics for Phase 1: 5-10 active distributor relationships across target markets, $500,000-$1M in annual revenue, and 3-5 reference customer deployments per market.

Phase 2: Strategic Expansion (Years 2-3) — Enter High-Growth Emerging Markets

Years 2-3 should target high-growth markets where Phase 1 certifications (FCC, CE) provide a regulatory foundation or require manageable incremental certification investment. The Middle East (Saudi Arabia, UAE) offers 15% CAGR growth driven by oil and gas digitization and smart city megaprojects. Certification requires CITC (Saudi Arabia) or TRA (UAE) approval, typically 4-8 weeks when leveraging existing CE test reports, with the requirement for a local representative or registered agent. Entry strategy should focus on exclusive distributor partnerships with companies that have existing relationships with Saudi Aramco, ADNOC, and major EPC (Engineering, Procurement, Construction) contractors.

Southeast Asia (Vietnam, Thailand, Indonesia) offers the highest growth rates in the Asia Pacific region (18-22% CAGR) with relatively accessible certification — many products can enter with CE or FCC certification plus local documentation supplements. Vietnam is particularly attractive due to its booming electronics manufacturing sector (Samsung, LG, Foxconn ecosystems) and its growing status as a supply chain alternative to China. Entry strategy should combine a local distributor for commercial coverage with a technical partnership for system integration support, as Southeast Asian customers often require higher levels of technical assistance than Western markets.

Latin America (Brazil, Chile, Colombia) should be approached selectively, focusing on mining and agriculture applications where these markets have the strongest demand. Brazil requires ANATEL certification (8-16 weeks, $8,000-$15,000) and is the gateway to the South American market due to its size and Mercosur trade agreement influence. The Brazilian market also requires careful pricing strategy due to high import duties (30-60%) — local assembly or partnership with a Brazilian manufacturer may be necessary for price-competitive market segments. Chile and Peru offer faster market entry (no local certification required for some product categories) and strong demand from the mining sector.

Phase 3: Full Global Coverage (Years 3-5) — Establish Presence in Regulated Markets

Years 3-5 should address the most challenging markets — China, Japan, and Korea — where local certification, relationship-based business development, and cultural adaptation require significant investment. China is the most challenging market for foreign wireless equipment manufacturers: CCC and SRRC certification requires in-country testing (10-16 weeks, $15,000-$25,000), 5GHz spectrum regulations restrict outdoor use, and business development requires guanxi-based relationship building that foreign companies typically lack. The recommended entry strategy for China is a joint venture with a local wireless equipment company that already holds CCC/SRRC certifications and has established distribution relationships. This approach reduces the certification timeline by leveraging the partner’s existing certifications for co-branded products.

Japan requires TELEC (MIC) certification (8-12 weeks) and presents unique market characteristics: the highest quality expectations globally (zero-defect mentality), preference for Japanese-language technical documentation and support, and multi-layered distribution (manufacturer → primary distributor → secondary distributor → reseller → end customer). The recommended entry strategy is to partner with a Japanese trading company (soga shosha) or specialized wireless distributor that can navigate the distribution structure and provide the required level of customer support.

South Korea requires KC certification (8-12 weeks) and offers opportunities in semiconductor manufacturing (Samsung, SK Hynix), shipbuilding, and smart factory automation. The Korean market is smaller than China or Japan but offers faster decision cycles and stronger adoption of new wireless technologies. Entry strategy should focus on a single exclusive distributor with technical capabilities in the target application segment (semiconductor factory automation is the highest-value segment).

Market Entry Methods — Matching Approach to Market Characteristics

The choice of market entry method — direct export, distributor partnership, joint venture, or local subsidiary — depends on market size, regulatory complexity, cultural distance, and the level of local support required. Using the wrong entry method for a given market is a common cause of failed international expansion.

| Entry Method | Investment Level | Control Level | Best For | Time to Revenue |

|---|---|---|---|---|

| Direct Export (B2B website + email) | Low ($10K-$30K) | High (direct customer relationships) | Initial market testing, niche products, repeat purchases | 1-3 months |

| Distributor Partnership | Moderate ($30K-$80K) | Medium (distributor manages local relationships) | Most markets, especially where local presence is required | 3-6 months |

| Joint Venture | High ($100K-$300K) | Shared (50/50 or majority control) | China, India, regulated markets requiring local entity | 6-12 months |

| Local Subsidiary | Very High ($300K-$1M+) | Full control | Major markets with sustained >$5M annual revenue | 6-18 months |

Partnership and Distribution Opportunities

Types of Global Partners — Mapping Partner Profile to Market Requirements

Different markets and customer segments require different types of partners, each with distinct capabilities, investment requirements, and go-to-market approaches. Selecting the wrong partner type for a given market is a common source of channel conflict and underperformance.

Regional Distributors maintain inventory, manage logistics, process credit, and provide first-line technical support. They are the most common and scalable partner model, suitable for markets where the product can be specified and deployed with standard configuration. The ideal distributor in industrial wireless has: existing relationships with system integrators and resellers in the target application vertical (factory automation, oil and gas, mining), technical staff who can configure and test wireless products, and a minimum annual revenue of $5M+ to ensure they have the resources to invest in inventory and training. Distributors typically require 30-45% gross margins and expect territory exclusivity for the first 12-24 months of the relationship.

System Integrators (SIs) design, install, and maintain complete wireless solutions for end customers. They are the appropriate partner model for complex deployments (multi-site mesh networks, long-range bridge links, private 5G networks) that require custom engineering. SIs typically specify equipment brands they trust and have trained their engineers on, making them a high-value channel to develop. The best SIs for industrial wireless partnerships have: wireless certifications (Cisco CWNA, Cambium CNP, or equivalent), experience in the target vertical (manufacturing, mining, oil and gas), and annual project revenue of $2M-$20M. SI partnerships require investment in training, joint reference development, and dedicated technical support.

OEM Partners integrate Zukaka’s motherboard platforms into their own branded products — adding enclosures, firmware customization, and certification under their own brand. This model is particularly effective for: companies in regulated markets (China, Japan, Brazil) that already hold local certifications and can rebadge Zukaka’s platforms with minimal additional certification cost, local brands in emerging markets that want wireless products under their own name without investing in RF design, and application-specific equipment manufacturers (surveillance, access control, industrial automation) that want to add wireless connectivity to their existing product lines. OEM partners require NDA, supply agreement, and quality specifications documentation.

Technology Partners integrate Zukaka’s wireless technology into complementary solutions: antenna manufacturers who optimize antenna designs for specific band plans, cloud platform providers who integrate device management into their IoT platforms, and chipset vendors who collaborate on reference designs. Technology partnerships are typically non-exclusive and focus on joint technical development rather than commercial distribution.

Partner Evaluation Criteria — Systematic Assessment Framework

A systematic partner evaluation framework prevents the common mistake of selecting partners based on enthusiasm and market access claims without verifying technical capability, financial stability, and strategic alignment. The following five criteria should be evaluated for each potential partner, with a minimum threshold score required for partnership initiation.

| Criterion | Weight | Minimum Threshold | Evaluation Method |

|---|---|---|---|

| Technical Capability | 25% | At least 2 staff with wireless networking certifications (CWNA, CNP, or equivalent RF training) | Interview technical team, review past wireless projects, request certification documentation |

| Market Coverage | 25% | Active relationships with 20+ end customers or 5+ active system integrators in target segments | Review customer list, speak with 3 reference customers, assess CRM pipeline |

| Financial Stability | 20% | Minimum $2M annual revenue, profitable for 2+ consecutive years, credit line of $200K+ | Review audited financial statements, obtain credit report, verify bank references |

| Support Infrastructure | 15% | Dedicated technical support staff, spare parts inventory, RMA process documentation | Audit support processes, test response times, visit warehouse facility |

| Brand & Cultural Alignment | 15% | Compatible market positioning, no conflicting product lines, English-language business capability | Review marketing materials, discuss target customer profile, assess communication responsiveness |

Distribution Strategy by Region — Recommended Channel Models

The optimal distribution model varies by region based on market maturity, customer purchasing behavior, and the level of technical support required. A regionally optimized channel strategy typically generates 20-40% higher revenue per distributor than a uniform global approach.

| Region | Recommended Channel Model | Rationale | Key Success Factors |

|---|---|---|---|

| North America | Two-tier distribution: National Distributor → Regional VARs/SIs | Mature distribution ecosystem; end customers expect local VAR support for installation and integration | Partner training program, joint marketing funds, lead registration system |

| Europe | Multi-country distributor with coverage in DE, UK, FR, BENELUX | Single distributor can cover 45%+ of European market; CE certification provides unified regulatory access | Multi-language support (EN+DE+FR), local stock in EU warehouse, 24h RMA turnaround |

| Asia Pacific | Country-specific exclusive distributors + technical partnership for integration | Relationship-driven markets require local partners with existing customer trust; technical support is critical | Local language documentation, in-country technical training, reference site visits |

| Middle East | Exclusive distributor per country (KSA, UAE, Qatar) with SI capabilities | Project-based demand requires partners who can manage multi-million dollar deployments; government relationships essential | Local registration, Arabic-speaking support, attendance at regional trade shows (GITEX, ADIPEC) |

| Latin America | Regional distributor covering Brazil + Spanish-speaking countries | Brazil (40% of regional market) requires ANATEL certification and local support; Spanish-speaking countries can be served from a single hub | Portuguese/Spanish support, ANATEL-certified inventory, regional stock in Miami or Sao Paulo free trade zone |

Frequently Asked Questions

Q: What is the total global market size for industrial wireless communication?

The global industrial wireless communication market is valued at approximately $15.8 billion in 2024 and is projected to exceed $35 billion by 2030, representing a compound annual growth rate (CAGR) of 14.2%. This growth is driven by three structural factors: the expansion of industrial IoT (37 billion connected devices expected by 2027), the transition from proprietary industrial protocols to IP-based wireless networking, and the declining cost of industrial-grade wireless hardware. The Asia Pacific region accounts for the largest share (41% at $6.5B), while the Middle East and Africa show the highest growth momentum driven by oil and gas digitization and smart city megaprojects.

Q: Which regions offer the best opportunities for industrial wireless solutions?

Asia Pacific offers the largest absolute market and highest growth rate (18% CAGR), while North America and Europe offer premium pricing and mature distribution ecosystems. Within Asia Pacific, China is the largest single market ($2.9B) but requires significant certification investment (CCC/SRRC) and relationship-based business development. Southeast Asian markets (Vietnam, Thailand, Indonesia) offer the highest growth rates (18-22% CAGR) with more accessible regulatory requirements. For companies seeking premium pricing and reference customers, the US ($4.2B) and Germany ($870M) are the best markets. For companies focused on natural resource applications, the Middle East (oil and gas) and Australia/Chile (mining) offer targeted high-value opportunities.

Q: What certifications are required for global market entry?

The essential certifications for global coverage are: FCC Part 15 (United States), CE RED 2014/53/EU (European Union), ISED RSS-247 (Canada), and ACMA RCM (Australia) as the foundational four. For expansion into Asia: CCC + SRRC (China), TELEC (Japan), and KC (Korea) are required but can be deferred to Phase 2 market entry. For emerging markets: ANATEL (Brazil), CITC (Saudi Arabia), and TRA (UAE) are typically required. The total certification investment for a single product platform across 5 major markets (US, EU, Canada, Australia, China) ranges from $50,000-$85,000 assuming pre-compliance screening catches 90%+ of issues before formal testing. A phased certification strategy that prioritizes FCC + CE (covering approximately 60% of global market value) and defers China/Japan/Korea to Years 2-3 is the most capital-efficient approach.

Q: How do I choose the right market entry strategy for my wireless product?

Market entry strategy should be determined by three factors: your available investment capital, the complexity of regulatory certification in each target market, and the level of local technical support required by customers in that market. For companies with under $100K international expansion budget, the recommended approach is direct export through distributors in 2-3 English-language markets with clear certification pathways (US, UK, Australia). For companies with $100K-$300K budget, add an exclusive distributor in the Middle East and a distributor/technical partner in Southeast Asia. For companies with $300K+ budget, consider a joint venture in China or a local subsidiary in a major European market. The most common mistake is attempting simultaneous entry into 5+ markets — this dilutes marketing investment, overwhelms the support team, and leads to poor partner relationships in all markets.

Q: What are the key differences in frequency regulations for 5GHz across regions?

The 5GHz band (5150-5850MHz) is the most fragmented spectrum globally, with significant differences in available sub-bands, output power limits, and DFS (Dynamic Frequency Selection) requirements that directly affect product design and performance. The US (FCC) offers the most favorable outdoor regime: up to 1W EIRP on UNII-3 (5725-5850MHz) without DFS requirement, enabling maximum range for point-to-point bridges. Europe (CE RED) requires both DFS and Transmit Power Control (TPC) on the 5470-5725MHz band, limits outdoor use on 5150-5350MHz, and restricts the 5725-5850MHz band to low power (25mW EIRP). China’s regulations are the most restrictive: outdoor wireless is effectively limited to 2.4GHz, as the 5GHz band (5150-5350MHz only) is restricted to indoor, low-power use. These differences mean that a bridge designed for maximum performance in the US market will not achieve the same range in European or Chinese markets without region-specific hardware.

Q: How long does it take to achieve global certification coverage?

A phased approach to global certification typically takes 6-10 months for foundational coverage (FCC + CE + ACMA), 12-18 months for expanded coverage (including Canada, Middle East, Latin America), and 24-36 months for full global coverage (including China, Japan, Korea). The certification timeline is determined primarily by: the number of regional variants required (a single hardware platform with firmware region-locking is fastest), the availability of pre-compliance testing (in-house testing reduces first-pass failure by 60-80%), and the requirement for in-country testing (China, Japan, and Brazil require local testing, adding 6-10 weeks per market). We recommend maintaining a rolling certification calendar where Phase 2 market certifications begin while Phase 1 markets are already generating revenue — this prevents certification from becoming a bottleneck to expansion.

Q: What partnership models work best for different global markets?

The most effective partnership model varies by market maturity: two-tier distribution (distributor + VAR) works best in North America and Europe, exclusive distributors with system integration capabilities work best in the Middle East and Latin America, and joint ventures or OEM partnerships work best in China, Japan, and other highly regulated markets. In all markets, the most successful partnerships share three characteristics: the partner has existing technical capability (certified engineers who can configure and troubleshoot wireless equipment), the partner has active customer relationships in the target application vertical (not just general IT distribution), and the partnership agreement defines clear territory, target customers, and performance milestones with a 12-month review period. Partnerships without specific performance commitments rarely succeed — both parties need measurable goals to justify the investment in training, inventory, and joint marketing.

By: Zukaka Engineering Team |

Last Updated: June 14, 2026 |

Connect on LinkedIn

⭐⭐⭐⭐⭐ OEM/ODM Partner

“Zukaka PCBA modules have been integral to our industrial wireless product line. The engineering team’s responsiveness and the modules’ reliability in harsh environments have made them our preferred supplier for three consecutive years.”

— VP of Engineering, Industrial Wireless Equipment Manufacturer

⭐⭐⭐⭐⭐ System Integrator

“We’ve integrated Zukaka wireless bridge PCBA into our smart city and industrial IoT deployments. The industrial temperature range and long-range capabilities have consistently exceeded our specifications.”

— Technical Director, Systems Integration Company

✔ Certifications: FCC, CE, RoHS compliant |

✔ Industrial temperature range -40 to +85 °C |

✔ IP65-rated for outdoor deployment

Contact our engineering team for customized PCBA solutions and technical support.